That's me in red!

“Congratulations, you just build a bank”.

That's me in red!

Clara wished to replicate in Brazil their already successful payments solution in Mexico, but due to differences in banking scenarios, a digital account in Brazil posed specific challenges and aimed to cater to a target audience already used to a higher standard in banking experience and leading digital accounts such as Nubank and most big banks.

Research, strategize and design a new digital account to help generate profitability for the company by increasing assets under management, with a focus on positioning Clara as an one-stop-shop for managing business expenses and performing payments, transfers and collecting.

I led the design, user testing and documentation of this project from end to end. I referred to my Design Lead for feedback, specially involving the product’s timeline and the previous payment initiatives, but ultimately was responsible for Conta Clara and related features as a whole.

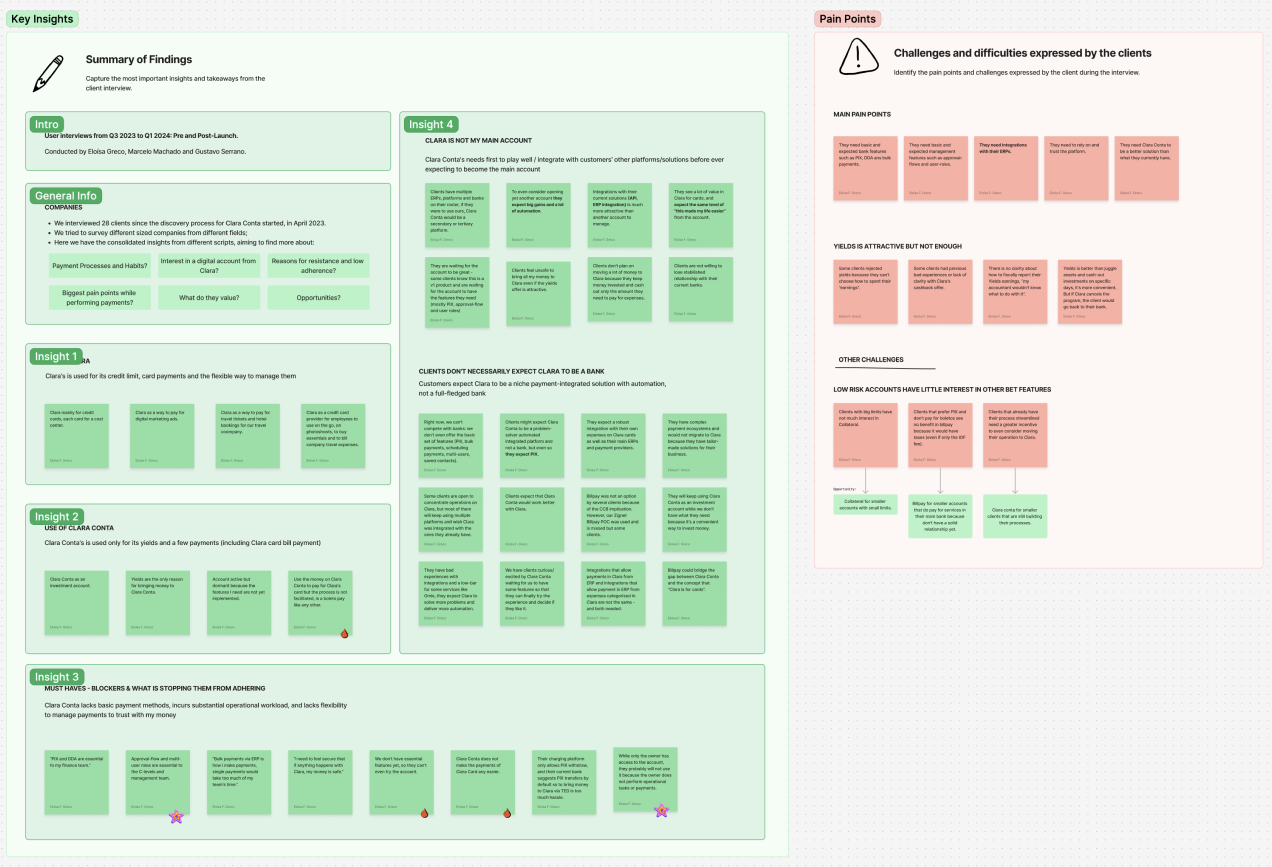

The first step on the discovery process was to understand the digital account customer, that had different needs and pain points from both the Mexican bill-pay users and the Brazilian corporate cards user. Also, it was important to educate Clara’s stakeholders on the omnipresence and symbolic importance of the Boleto as an payment instrument in Brazil.

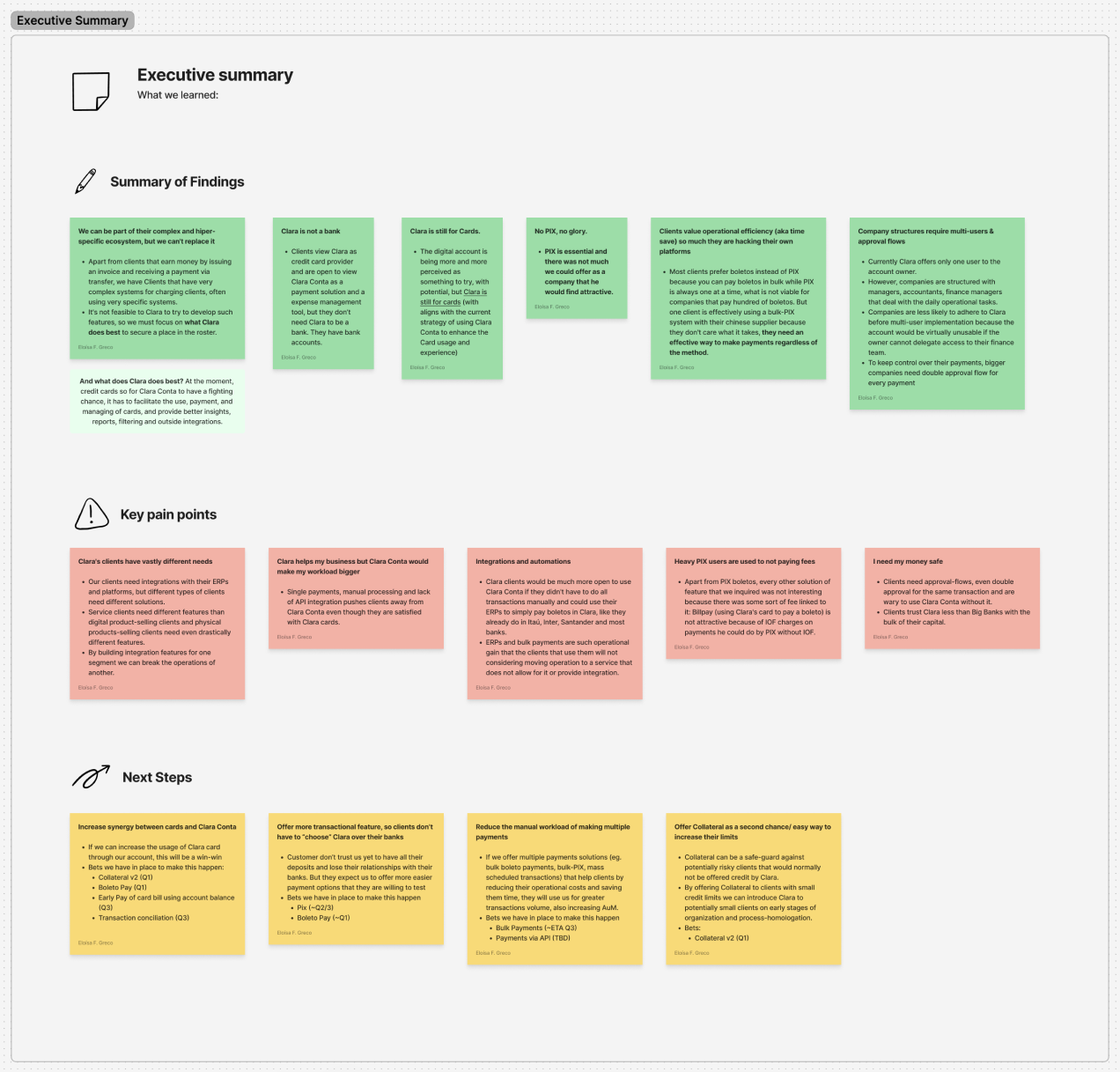

Research insights & findings.

Research insights & findings.

Quantitative research

200+ Customer surveys

Collaboration between design and data teams

Fullstory analysis

Qualitative research

10 client interviews

Internal investigation with our own financing and accounts payable teams

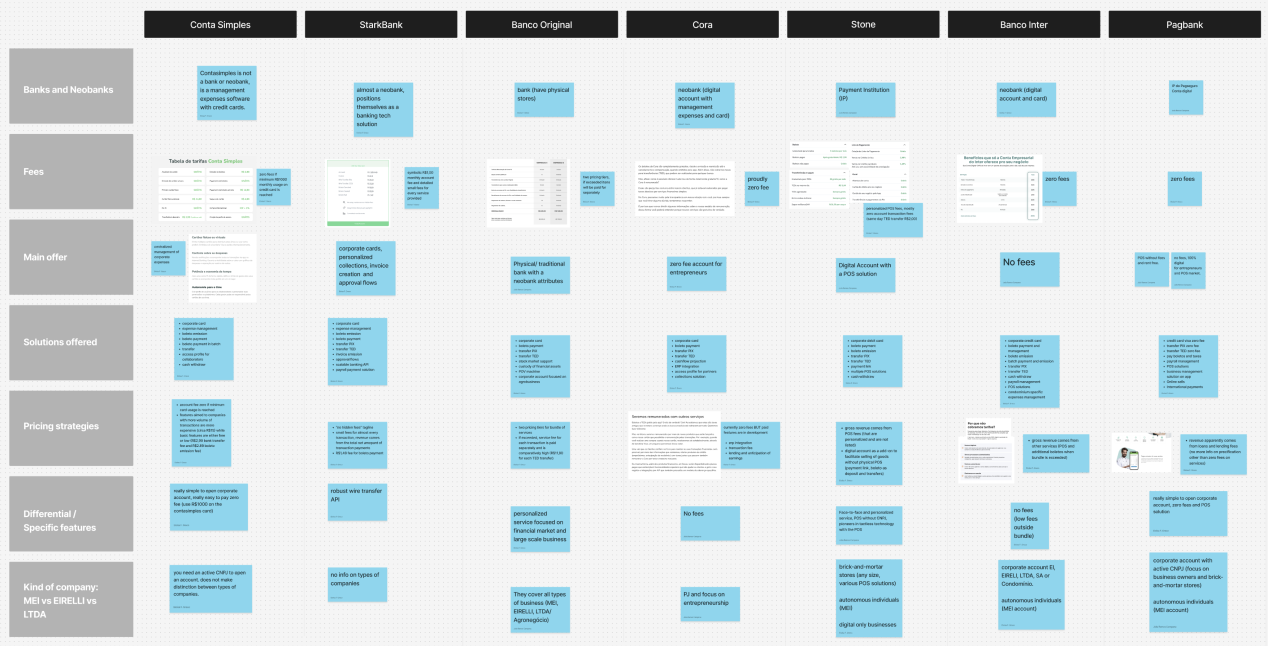

Banking benchmarks

Multiple Brazilian banks and payment products analyzed

Informed product decision regarding pricing, services and fees

To meet the expectations of stakeholders about the discovery process of the digital account, it was made an extensive research process focused on understanding priorities, deal-breakers and ultimately guide our product according to what our users needed, instead of what we wanted them to adopt.

• Multiple personas and ideal users: the digital account can be used by financing analysts, accountants, CFOs and CEOs - depending of the size of the company the degree of their stablished payment processes.

• The Brazilian market is used to high-level banking solutions and has a wide array of choices outside Clara.

• Users excited about translating the Clara Card experience to payments.

• Users excited about paying Clara Card using their own funds already in Clara’s digital account.

We knew our V1 product would be scaled down and bare-boned, so we prioritized building solid basics instead of more sophisticated product features. One of our main discoveries was that we could not compete with big banks and their relationship with our customers, so we aimed to be one of the products in their stack of expenses management workflow.

After presenting our insights to stakeholders, we worked with product defining the product strategy.

• We have to communicate with the business owner that doesn’t have an ERP solution yet. This ended up being key to guiding product to pursue more start-up instead of enterprise clients.

• They need a digital account because not every company expense is on a credit-card, such as paying tolls, buying props for photoshoots and buying water from street vendors.

• When surveyed, our clients responded they would prefer to pay a monthly fee for a bundle of services instead of per-transaction. We then proposed a fremium pricing strategy.

• Bring the Clara experience to transfers and boleto payments.

• Reuse components from payments Mexico, adapted to Brazilian needs and flows.

• Be sure to integrate the Card experience with the digital account to create a cohesive ecosystem.

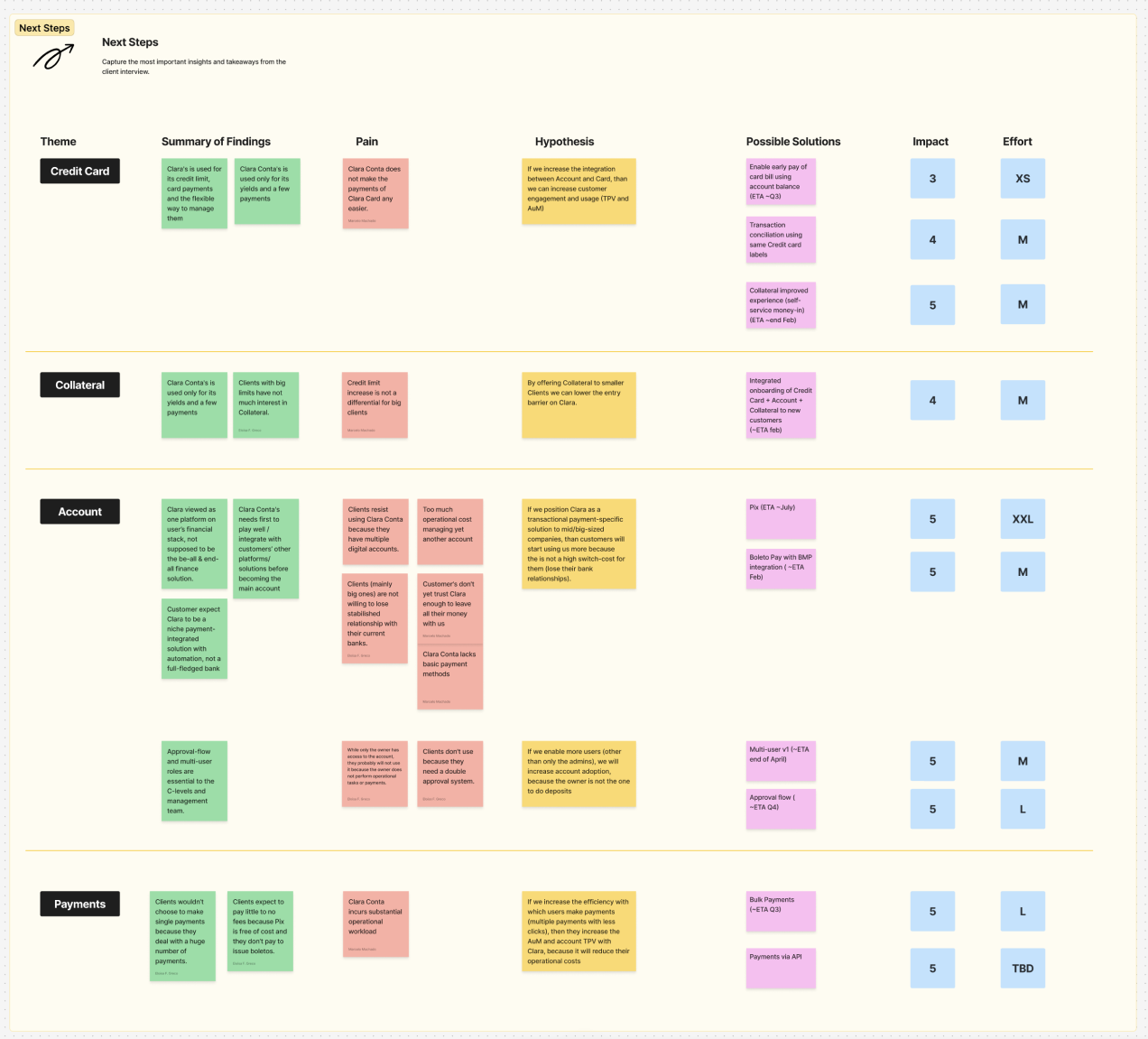

After reaching a bigger understanding about our user needs and pain-points, our team worked together to prioritize the features of our V1 launch.

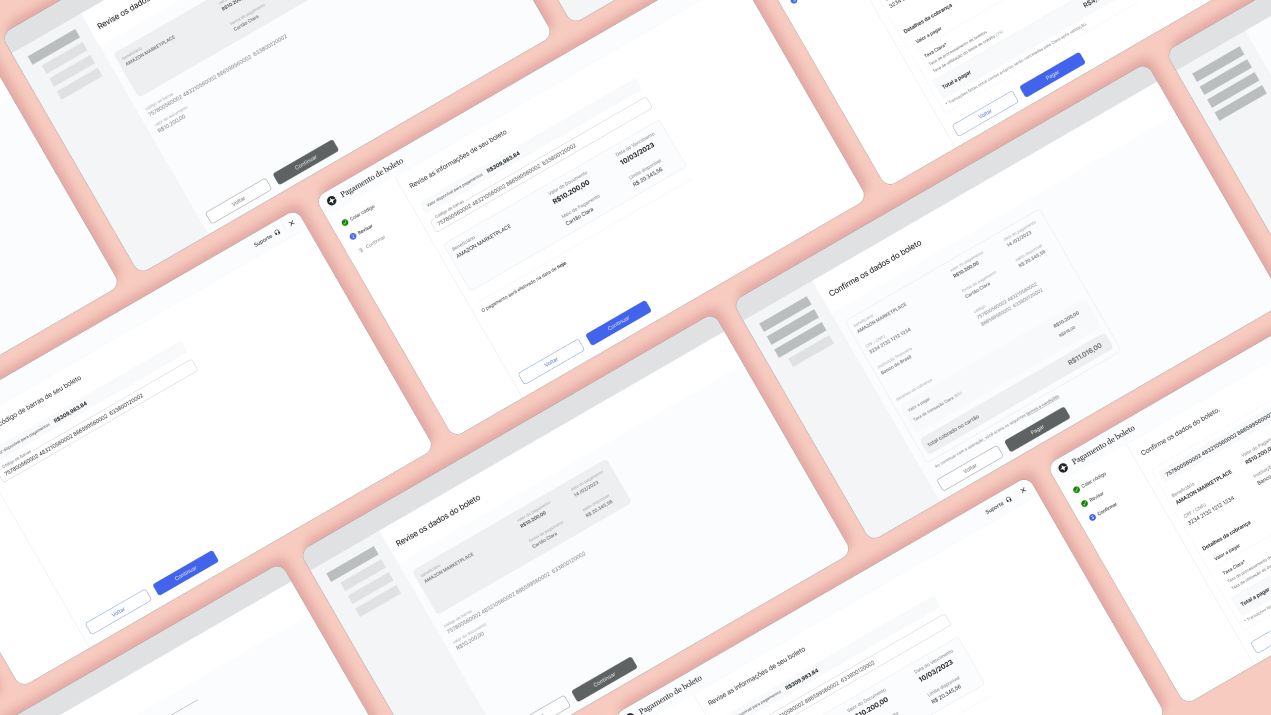

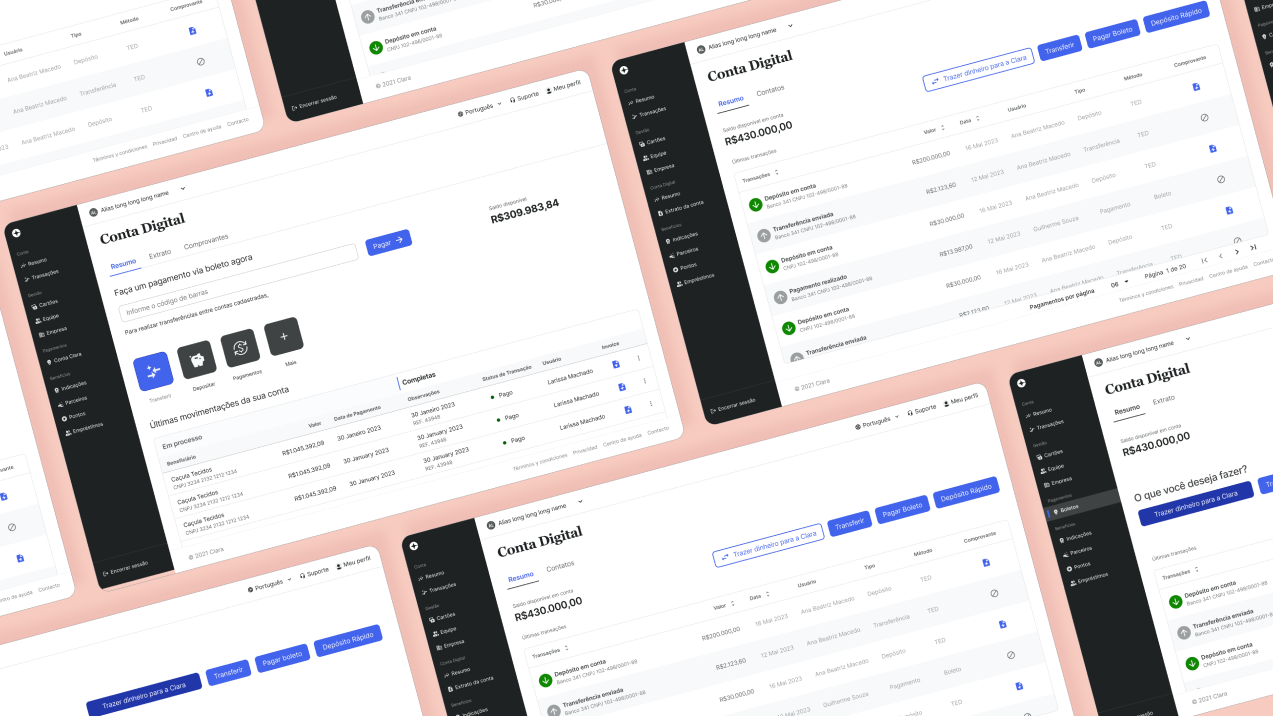

Examples of the Boleto Payment flow in both lo-fi and mid-fi mockups.

Time constraints and dependencies had an impact in our design, imposing significant limitations. But once design, engineering and product agreed on a bare-boned deliverable as a proof-of-concept, we got to work on the first mock-ups and prototypes.

• Moved forward with the components and made the specific adjustments relating to Brazilian ecosystem (for example, suggested longer input fields to fit barcode numbers)

• Stablished a visual design language cohesive with the other products from the company, aligned with constraints from payment partners.

• Focused on a robust table data filtering system instead of more banking-adjacent features (such as bulk payments or DDA) to be more aligned with the core value of the company: empower companies to have more clarity of their expense processes.

Validated all user flows for transactions;

Pushed for a security checkpoint;

Cohesive with Clara’s design system.

Examples the wireframe stage of the flow and some notes.

How to present the action items for the transactions? Single page or tabs system? What to have on the Digital Account home?

All those questions were constantly taken into consideration and a diverse array of iterations, explorations and proposals were discussed and approved with the engineering and product leads.

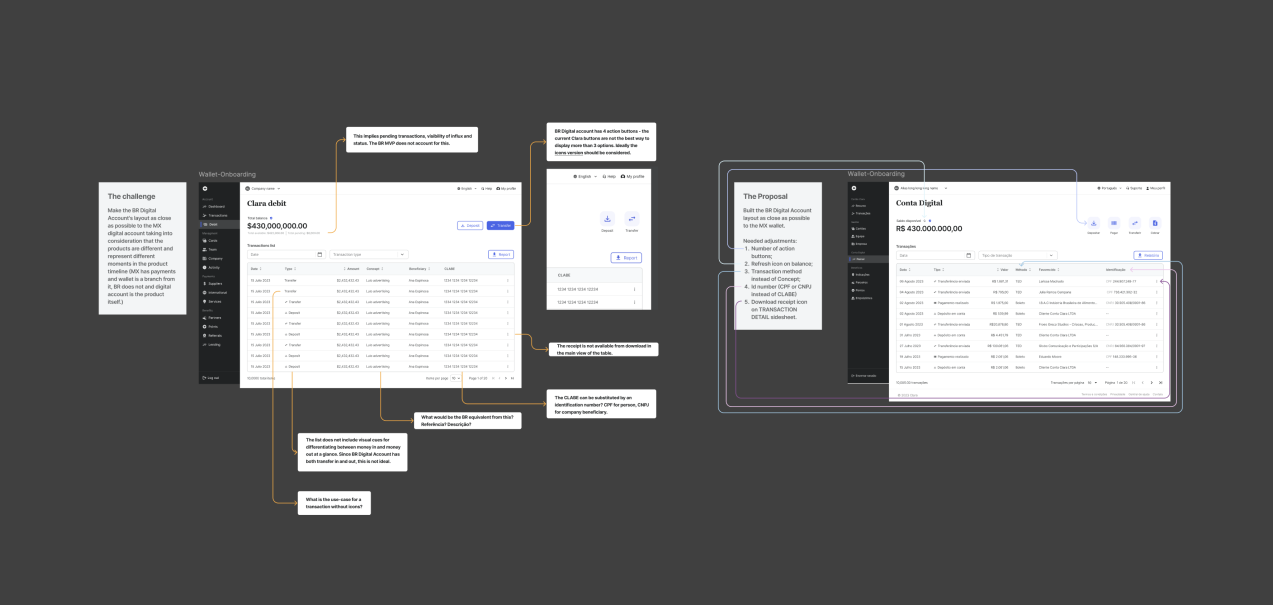

International stakeholders were anxious about the Brazilian product diverging too much from the Mexican product, which limited the solutions.

The product’s launch was scheduled to happen amidst a company wide UI redesign, which posed a series of challenges regarding dependencies between teams.

Director of Design and my Design lead laid off before launch. Suddenly I was the sole responsible for this product, interfacing with all stakeholders, responsible not only for the deliverables, research and quality-assurance, but for negotiating features, deadlines and expectations.

Explorations of compromises between MX and BR products.

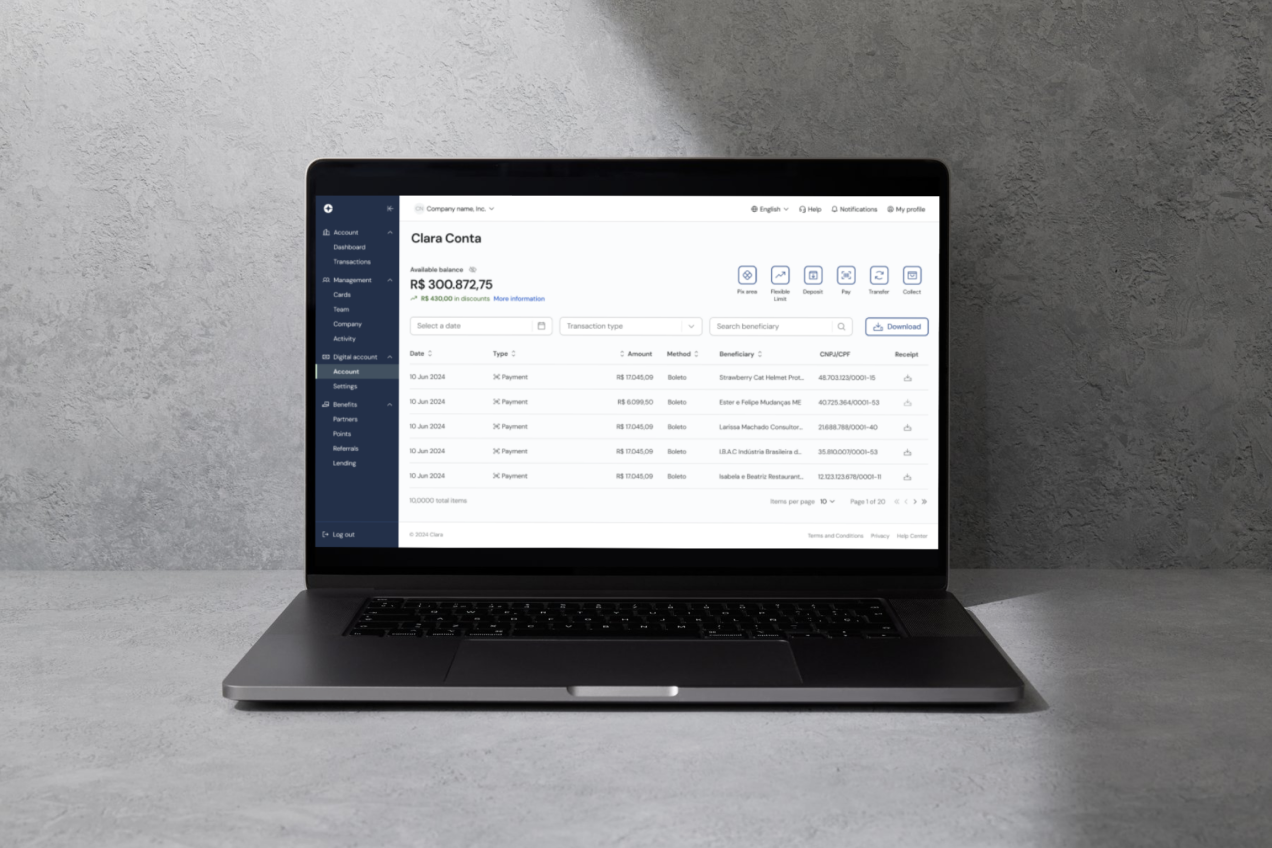

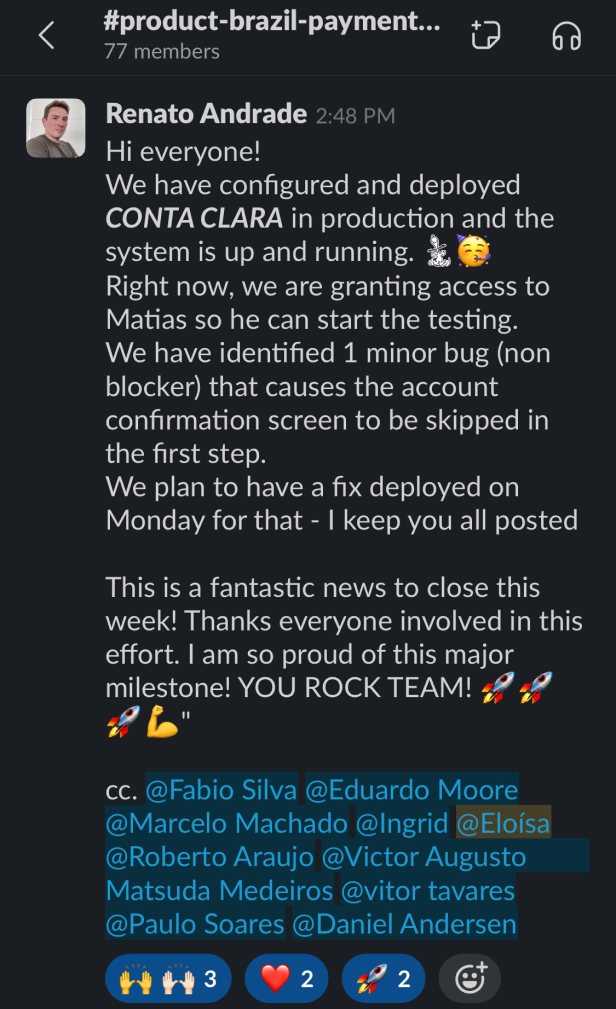

We successfully launched Clara Conta in November 2023, first for friends and family and soon after for the whole client base.

The launch was smooth with planned sessions for bug fixing and iterations; After one week, we had mapped a significant rate of opened accounts (2x the goal). We started working on the digital accounts next bets right away: Pix and Bulk Payments.

Test launch Slack communication.

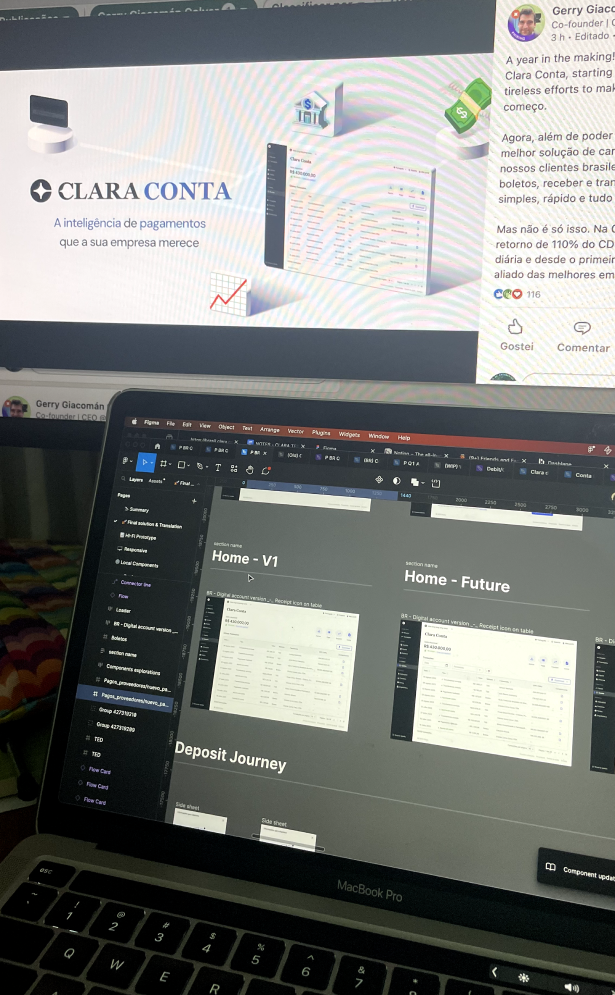

Launch posted by CEO on LinkedIn.

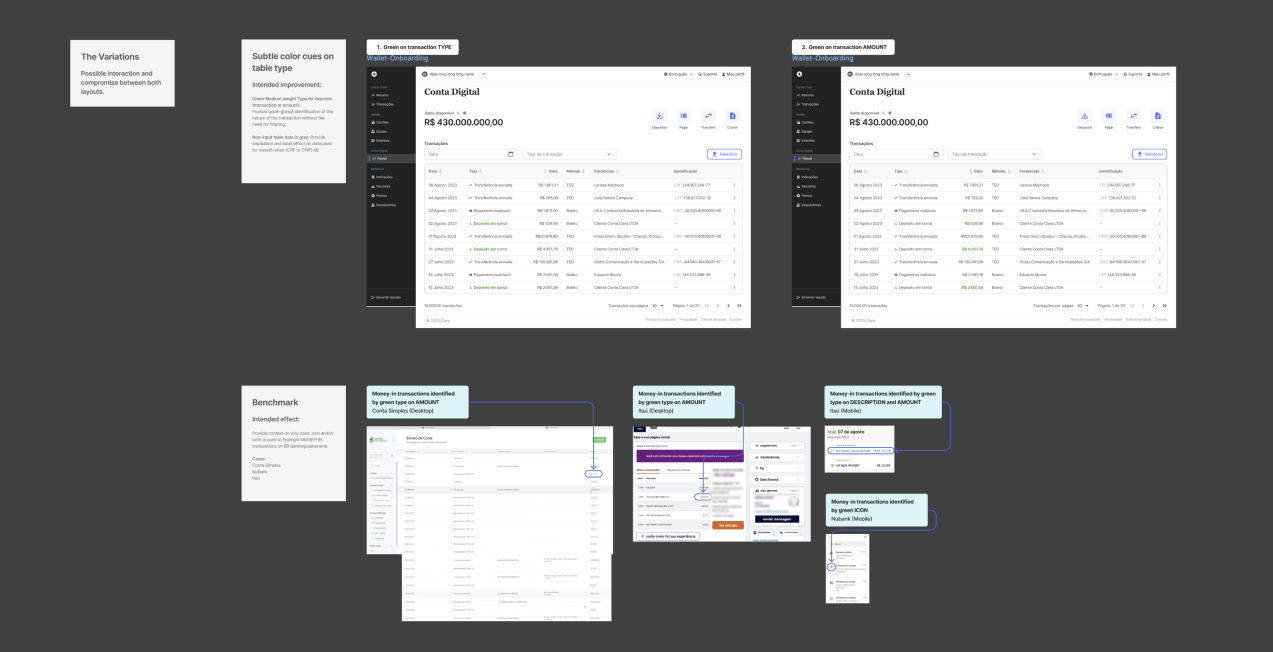

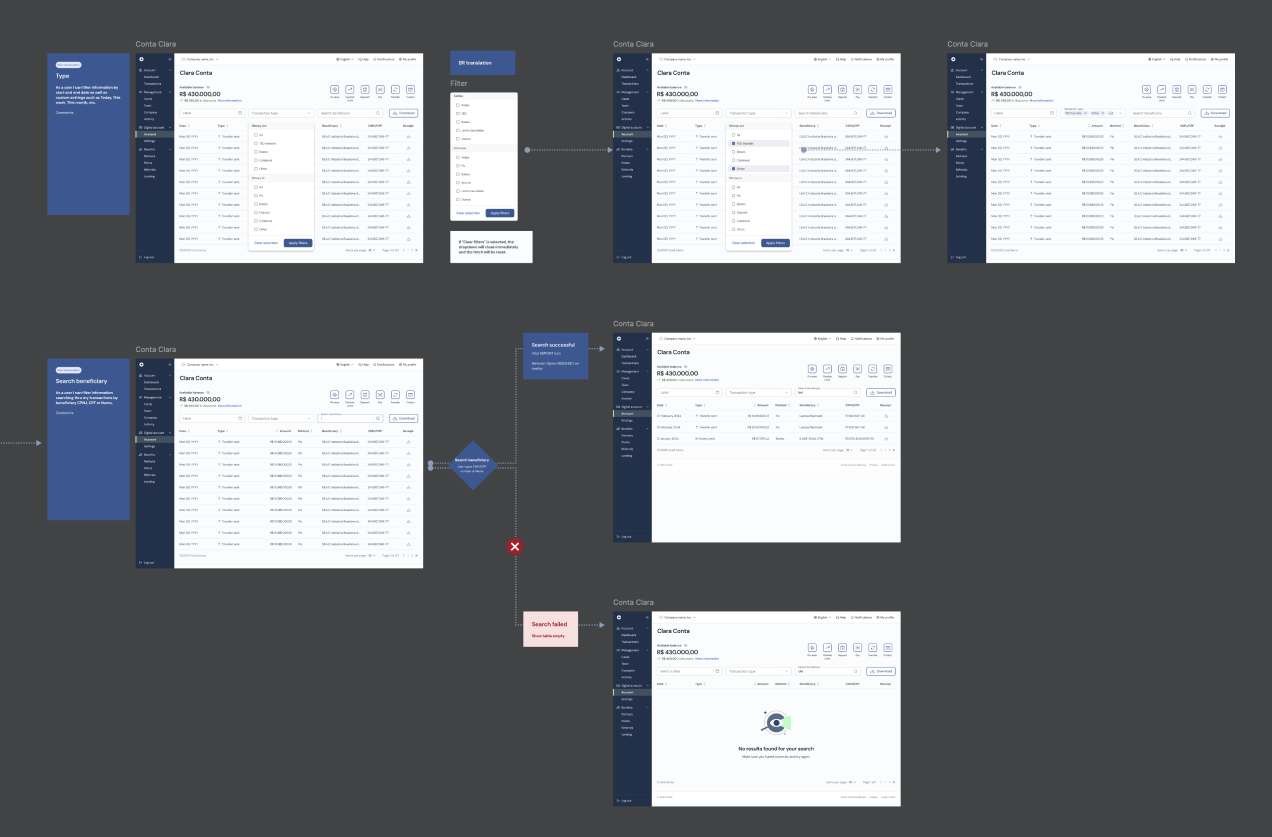

Mapping of Filters, parameters and options.

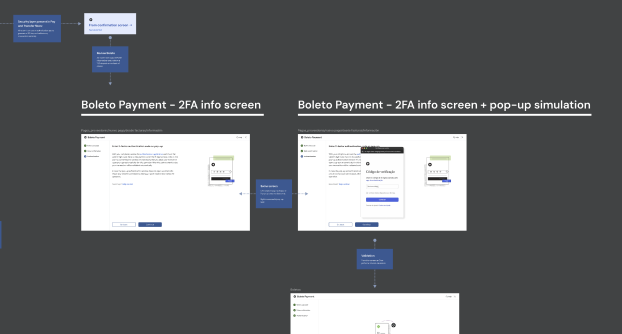

• My biggest contribution to Clara Conta was getting stakeholder buy-in for a security checkpoint.

• Because of differences between countries culture and banking scenario, the payment product in Mexico did not use a password confirmation before validating an operation.

• Surprisingly, ensuring Clara Conta would have a security layer (a pin, a one-time password, a 2FA code, anything) was my biggest fight and having this feature approved was my biggest achievement within the project.

• My designs for 2FA inputs and OTP code validation were included on the company’s design system, since there wasn’t a security checkpoint for operations before the digital account. Ultimately, the team went with a pop-up solution that required a screen on its own.

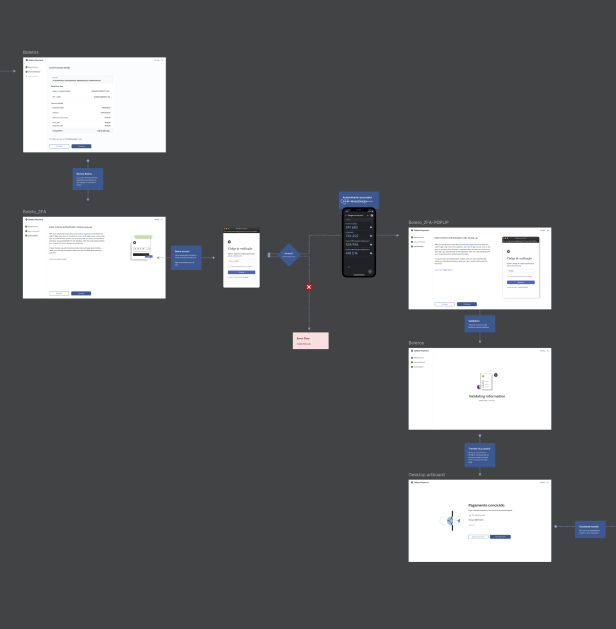

Security layer mock-up on Masterfile.

Security layer mock-ups on approval files.

LinkedIn banner from launch.

The name “ClaraConta” was short-lived and replaced with Clara’s Digital Account - we can see on the Portuguese version of the launch announcement that it was already starting to be phased-out.

Team Clara Brasil at Holiday Office Party, 2023.

LinkedIn article on the account, by the Lead Product Owner.